For many CTA employees, the frustration surrounding the pension system is not just about the future — it is about watching their paycheck contributions steadily climb year after year.

Over the last two decades, employee pension contributions have increased dramatically. In 2007, CTA employees contributed 3% of their wages toward their pension. Since then, that percentage has climbed through a series of increases:

- 2007: 3%

- 2008: 6%

- 2010: 8.34%

- 2012: 8.65%

- 2014: 10.12%

- 2017: 11.96%

- 2018: 12.01%

- 2018: 13.32%

- 2024: 13.795%

That represents an increase of roughly 400% from where contributions started.

For many frontline employees — bus operators, rail operators, mechanics, and other CTA workers — these increases represent a significant reduction in take-home pay. Many employees feel they are being asked to carry a larger and larger share of the burden for decisions made long before they had a seat at the table.

The question is simple:

Can a pension be financially healthy without continuously reaching deeper into employees’ pockets?

The answer is yes.

The math can work — when everyone pays their fair share.

A Sustainable Pension Does Not Require Endless Employee Increases

A pension system succeeds when there is a balance between three key factors:

- Employee contributions

- Employer contributions

- Long-term investment growth

A properly structured pension plan does not depend on one group constantly making up for past mistakes, poor decisions, or years of underfunding. It depends on consistent contributions and responsible management.

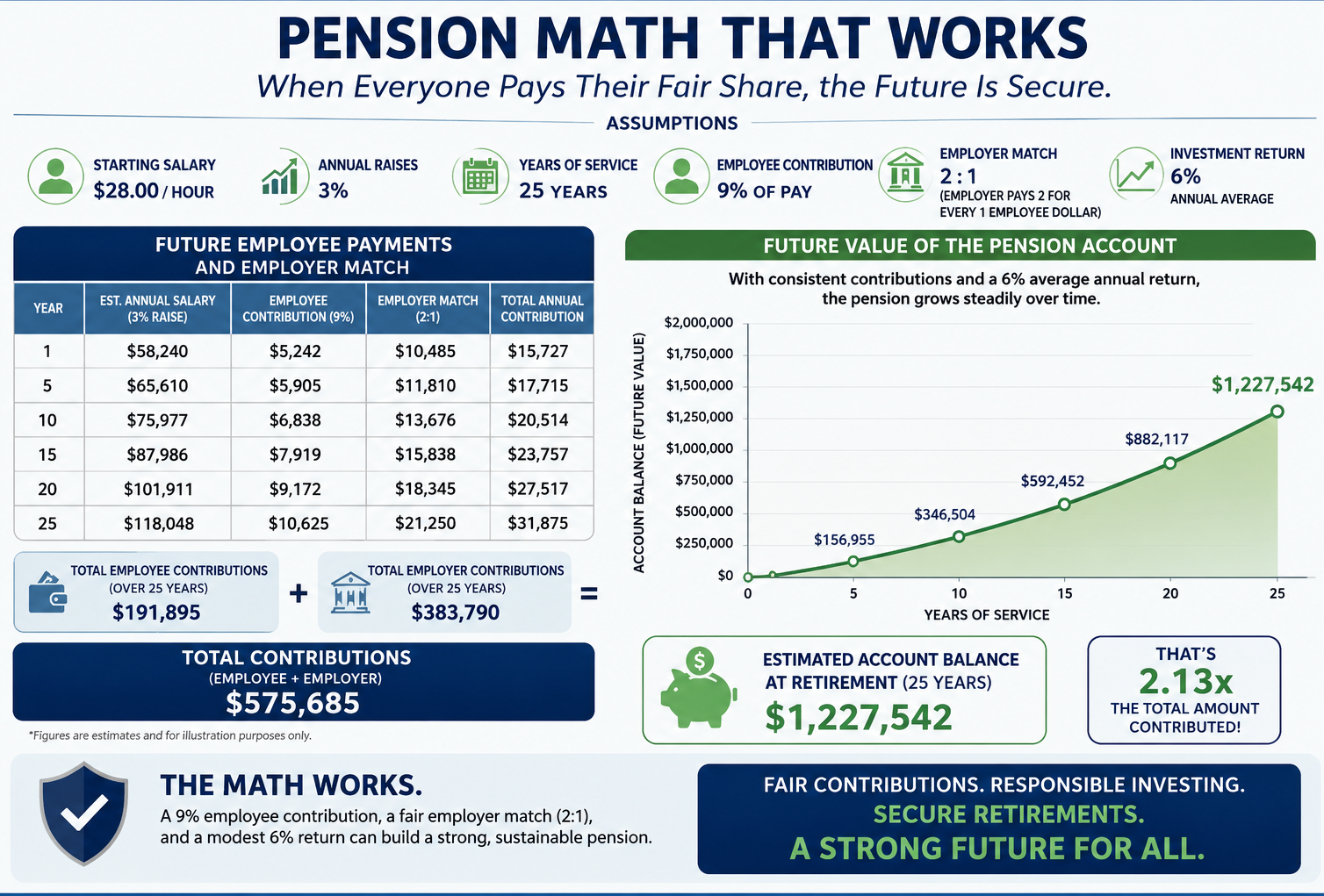

Consider a realistic example:

- Starting wage: $28 per hour

- Annual raises: 3%

- Career length: 25 years

- Employee contribution: 9%

- Employer match: 2-to-1

- Average investment return: low 6% annually

Under these assumptions, the pension system has the ability to build a strong financial foundation.

The employee contributes consistently throughout their career. The employer contributes its required share. The money is invested responsibly over time. The power of compound growth does what it is supposed to do.

That is how pensions were designed to work.

The Problem Is Not the Worker

CTA employees did not create decades of pension challenges. They did not make funding decisions decades ago. They did not control investment choices, benefit structures, or financial management decisions.

Yet, year after year, employees have been asked to contribute more.

At some point, a question must be asked:

Should the lowest-paid employees continue to be treated as the solution to every pension problem?

A pension system should not function like a piggy bank where workers constantly fill the gap created by larger financial failures.

A healthy pension requires accountability at every level.

Fair Contributions Create Stronger Pensions

The goal should not be to reduce retirement security. The goal should be to protect it.

A fair system means:

- Employees contribute a reasonable and predictable amount.

- Employers meet their obligations.

- Pension funds are managed responsibly.

- Long-term assumptions are realistic.

- Future retirees are protected.

A 9% employee contribution, combined with a fair employer match and responsible investment returns, demonstrates that there is a path forward.

The solution is not endless increases on the backs of workers.

The solution is better pension math.

How the Pension Math Works: The Numbers Behind the Growth

The purpose of this example is to show what happens when employees contribute a fair amount, the employer contributes its share, and pension funds are invested responsibly over time.

Year 1: Starting the Pension

A new employee earning approximately $28 per hour earns about $58,240 per year.

At a 9% employee contribution rate, the employee contributes:

Employee contribution: $5,242 per year

With a 2-to-1 employer match, the employer contributes:

Employer contribution: $10,485 per year

Total money added to the pension:

$15,727 in the first year

The employee puts in one dollar, and the employer adds two dollars.

Year 5: Growth Begins

After annual raises of 3%, the employee’s salary grows to about:

$65,610 per year

Employee contribution:

$5,905

Employer contribution:

$11,810

Total annual contribution:

$17,715

By this point, the account is no longer growing only from contributions — investment returns begin adding significant value.

Year 10: The Power of Compound Growth

After 10 years:

Salary grows to approximately:

$75,977

Annual employee contribution:

$6,838

Annual employer contribution:

$13,676

Total added that year:

$20,514

The pension account is estimated to grow to approximately:

$346,504

The important point: the account is growing faster because earlier contributions have had years to earn investment returns.

Year 15: Growth Accelerates

At year 15:

Salary:

$87,986

Employee contribution:

$7,919

Employer contribution:

$15,838

Total annual contribution:

$23,757

Estimated account value:

$592,452

The investment earnings are now becoming a major part of the pension growth.

Year 20: Returns Become a Major Factor

At year 20:

Salary:

$101,911

Employee contribution:

$9,172

Employer contribution:

$18,345

Total annual contribution:

$27,517

Estimated account value:

$882,117

At this stage, the pension is benefiting from decades of contributions and compounding.

Year 25: Retirement Point

After 25 years:

Salary:

$118,048

Employee contribution:

$10,625

Employer contribution:

$21,250

Total annual contribution:

$31,875

Over the entire career:

Employee contributions:

Approximately $191,895

Employer contributions:

Approximately $383,790

Total contributions:

Approximately $575,685

With an average 6% annual investment return, the estimated pension account value grows to:

Approximately $1,227,542

That means the investment growth adds roughly:

$651,857 above the total contributions

The Main Point

The example shows that a pension does not need unlimited employee deductions to survive.

A balanced approach works:

- Employees contribute a predictable amount

- Employers contribute their fair share

- Investments earn reasonable long-term returns

- Funds are managed responsibly

The math works when everyone participates.

A sustainable pension is built through fairness, consistency, and responsible management — not by continually increasing the burden on employees.

No responses yet